"We'd been putting off transfer pricing documentation for two years because every quote we got was $50K and six months. Commenda had our Master File and two Local Files done in under a month. We didn't believe the timeline until we saw the draft."

Your TP policy. Documented.

Defensible. Done.

Transfer pricing policy, benchmarking, documentation, and filing — in weeks, not months, and at a fraction of what your Big Four firm quoted. OECD-aligned.

Trusted by global businesses

OECD BEPS has rewritten the global TP rulebook. Tax authorities in the US, UK, EU, India, and Australia have all expanded their transfer pricing audit programs in the last three years. The days of informal intercompany arrangements holding up under scrutiny are over.

Undocumented transactions are audit magnets

Without a contemporaneous documentation package, your intercompany pricing is presumed wrong. The burden of proof shifts to you — and "we used the same rate as last year" is not a defence.

BEPS Pillar Two is changing the calculus

The 15% global minimum tax means intercompany structures that were tax-efficient two years ago may now attract scrutiny from multiple jurisdictions simultaneously. Your documentation needs to account for this.

Penalties are specific and enforced

Transfer pricing penalties in most jurisdictions are calculated as a percentage of the adjustment — not a flat fine. The IRS can impose penalties of 20–40% of the underpayment. HMRC has similar powers. This is not a theoretical risk.

Your documentation is probably stale

Most companies that have transfer pricing documentation got it done two or three years ago with a Big Four firm and haven't updated it since. The policy that covered your business then almost certainly doesn't cover it now.

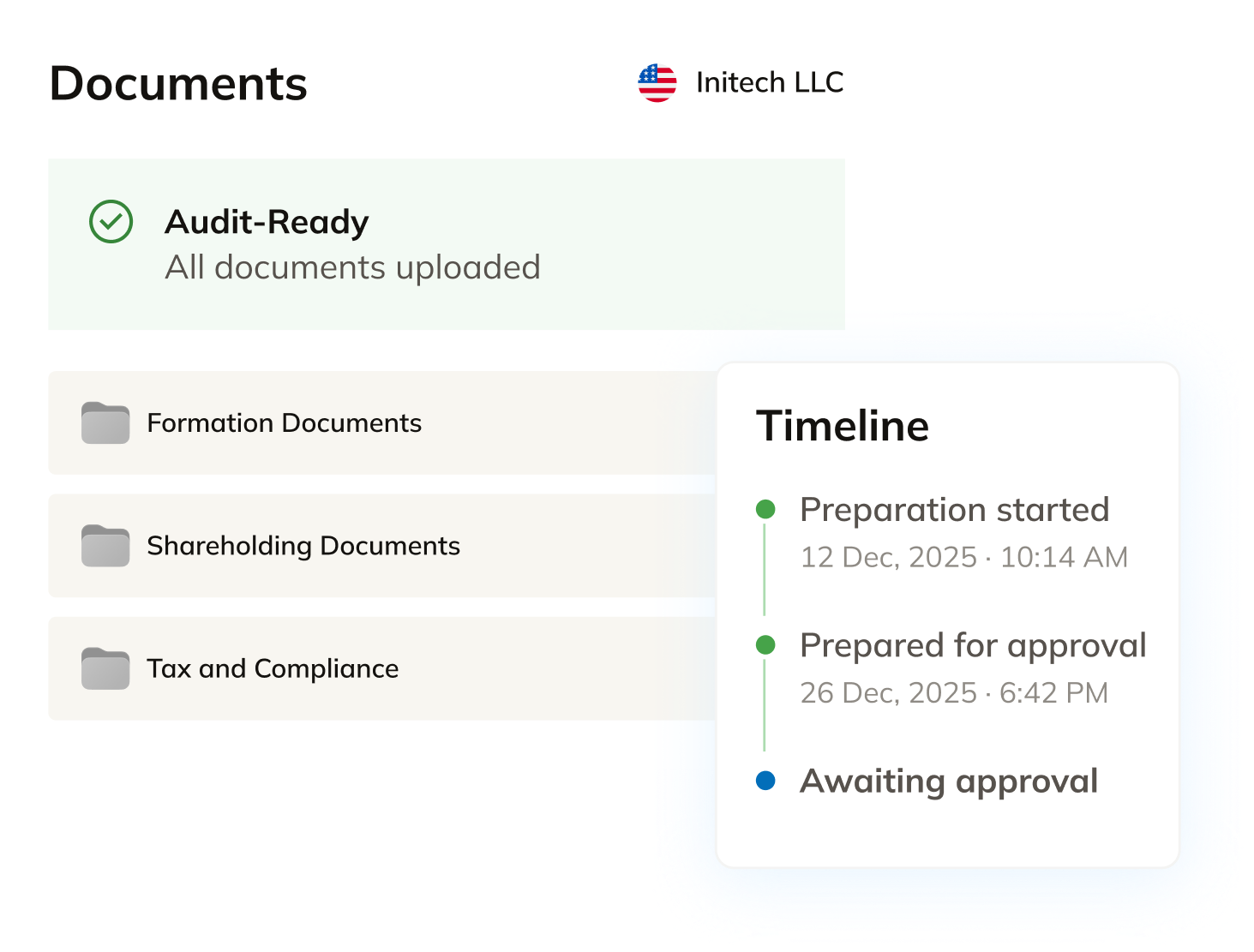

What Commenda does

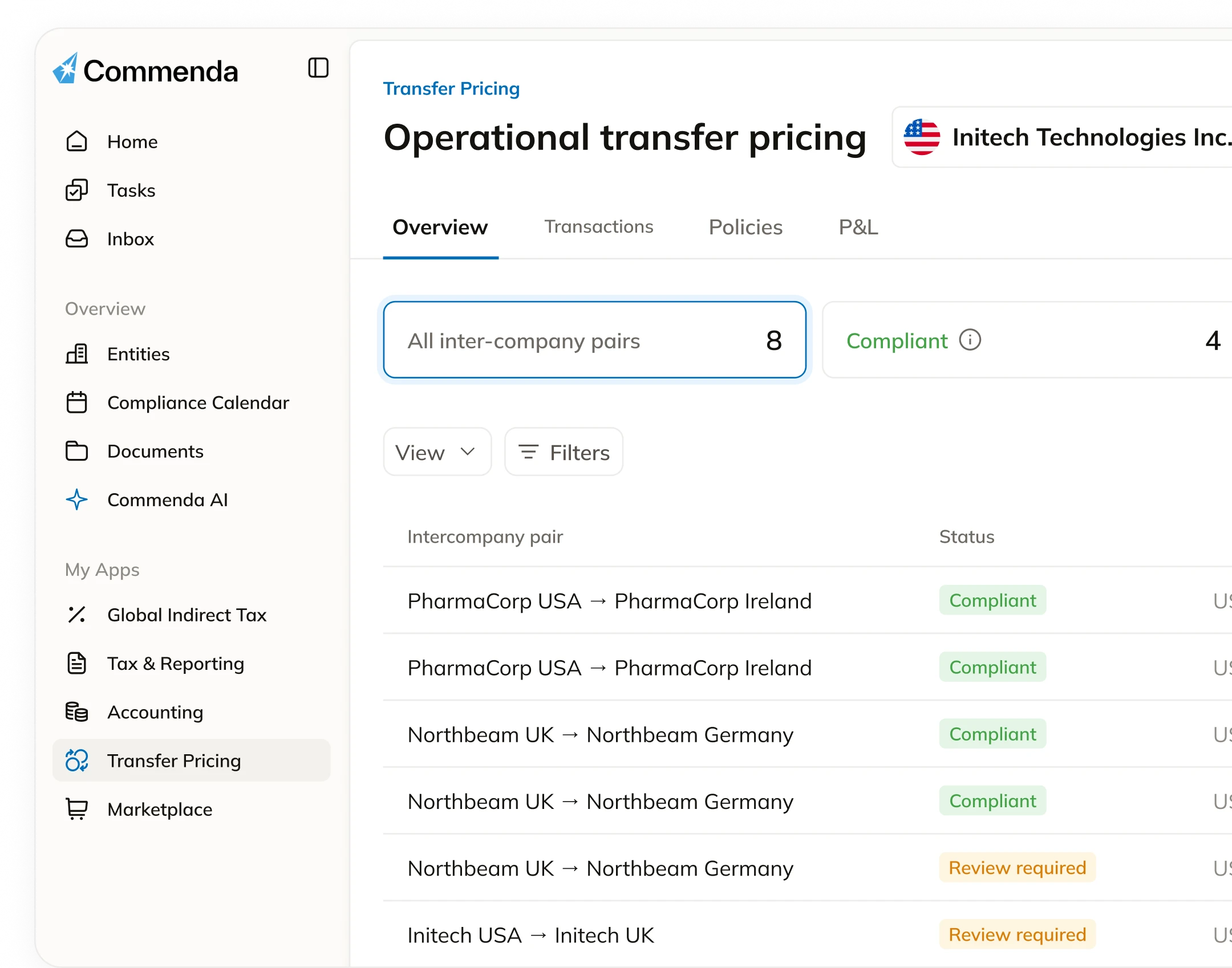

Commenda covers the full transfer pricing lifecycle — not just the documentation package that sits in a folder until your auditors ask for it. Policy, benchmarking, intercompany agreements, documentation, and filing. All maintained. All current. All connected to your ERP.

01 — Transfer Pricing Policy

Commenda builds your intercompany pricing policy against your actual entity structure, transaction types, and business model.

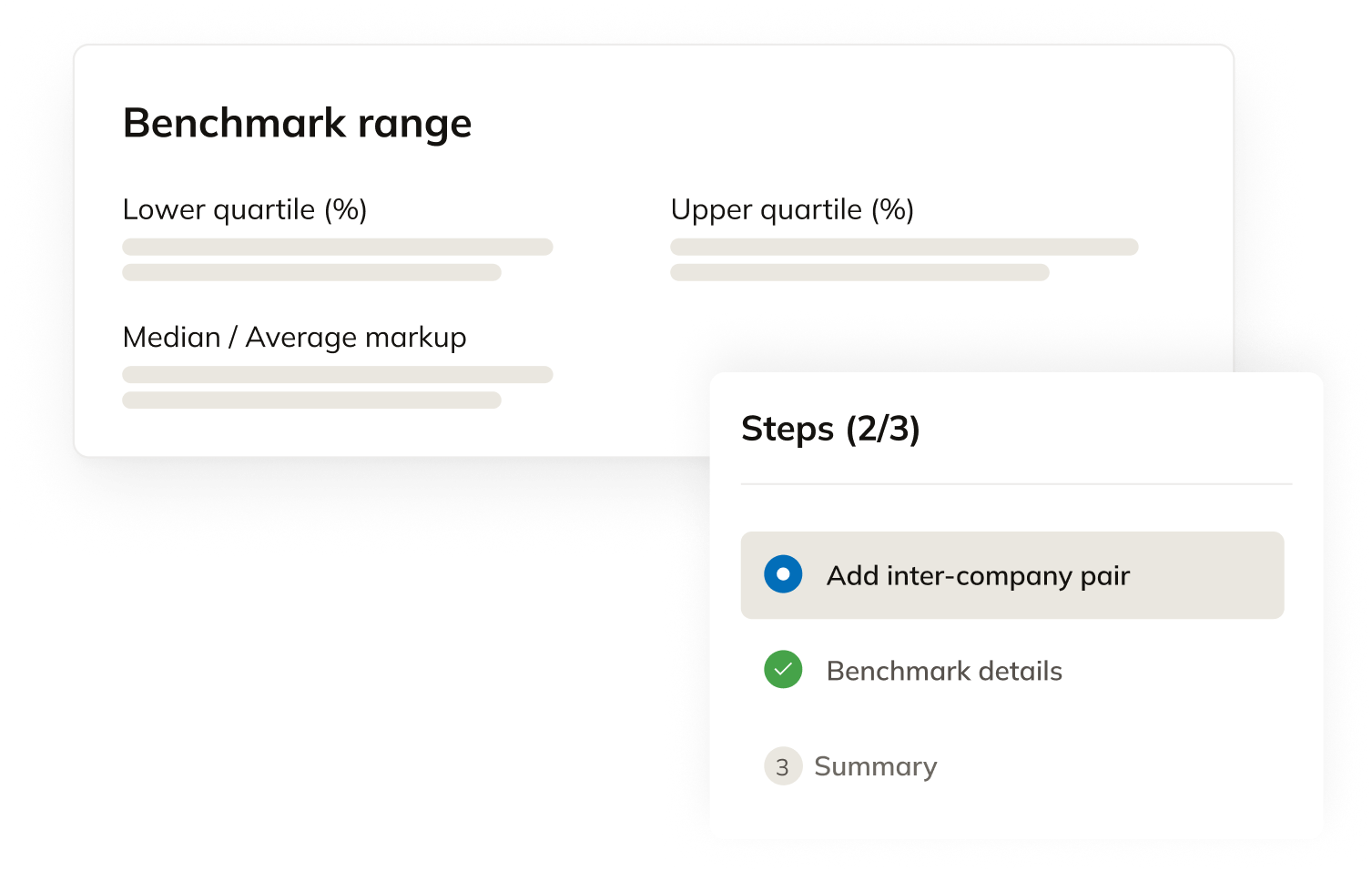

02 — Benchmarking

Commenda's benchmarking analysis pulls from commercial databases to establish comparable uncontrolled transactions for each intercompany arrangement.

03 — Documentation

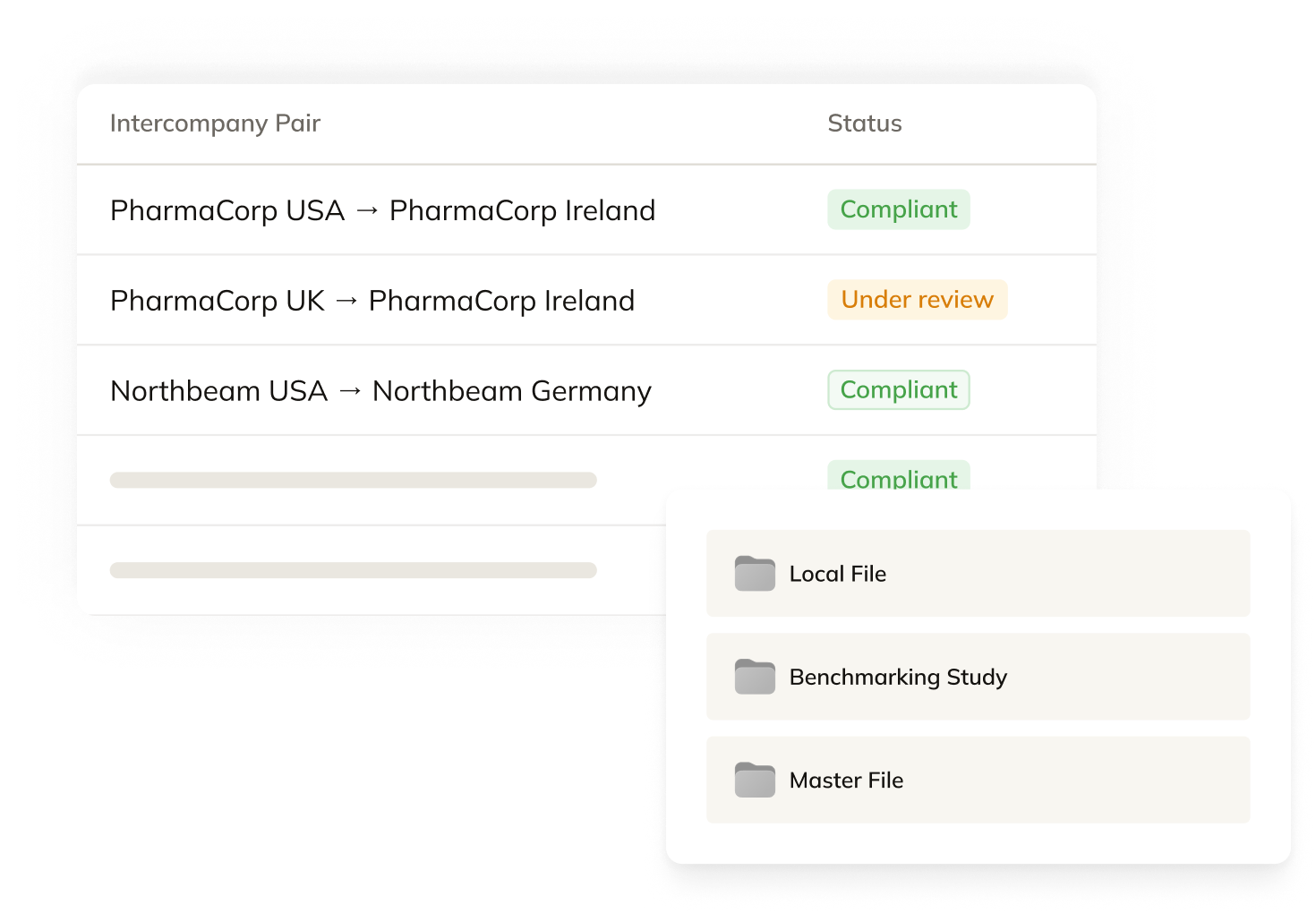

Commenda produces your full documentation package including Master File covering the group, Local Files per jurisdiction, and Country-by-Country Report where applicable.

04 — Filing & Ongoing Compliance

Commenda tracks every TP-related filing deadline across your entity footprint, prepares the required disclosures, and files.

This isn't about whether advisors have expertise — they do. It's about whether expertise should cost $60K and take six months for work that a systematized platform delivers in four weeks.

Big Four / boutique TP advisory

Expertise without infrastructure.

Commenda

Infrastructure with expertise built in.

"We'd been putting off transfer pricing documentation for two years because every quote we got was $50K and six months. Commenda had our Master File and two Local Files done in under a month. We didn't believe the timeline until we saw the draft."

"Our intercompany arrangements had evolved significantly since we last documented them. Three new entities, new transaction types, new jurisdictions. Commenda mapped the whole thing and rebuilt the policy from scratch in three weeks."

"The thing that surprised us most was how the TP documentation connected to the rest of our compliance stack. When we changed an entity's function, Commenda flagged the TP implications automatically. Our Big Four firm would have charged us for that call."

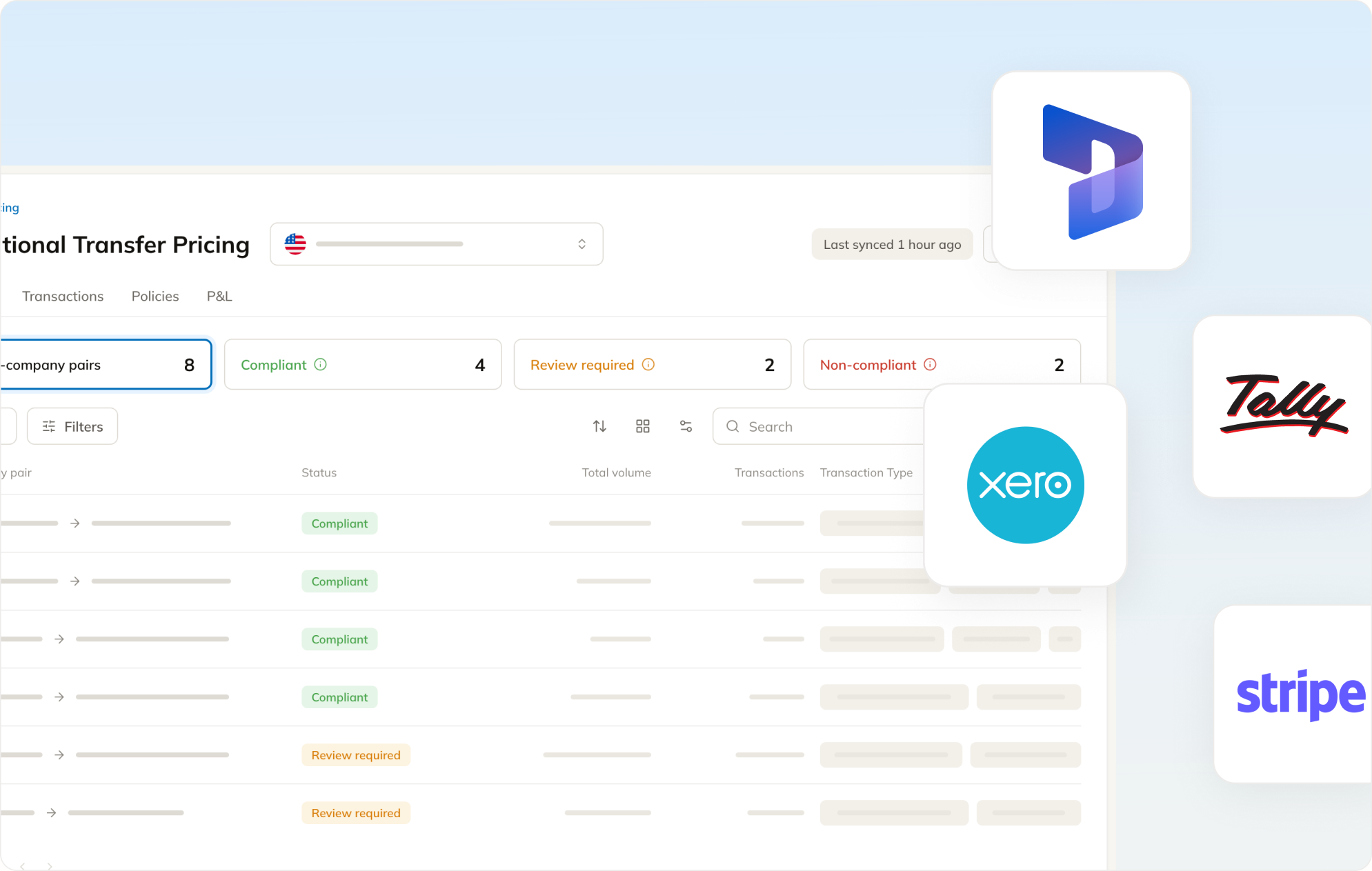

Integrations

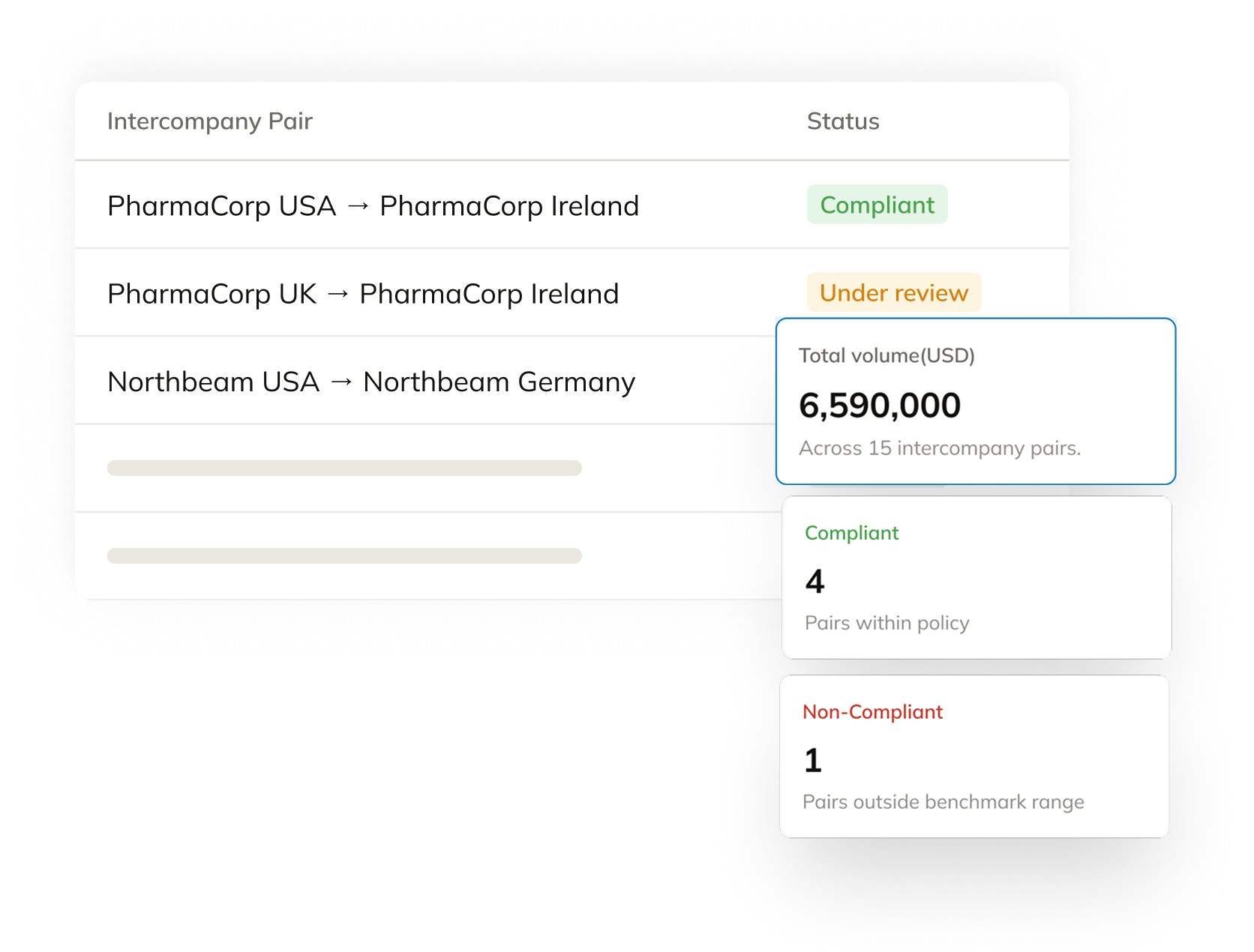

Your policy sets the prices and margins your entities are meant to follow. Commenda pulls intercompany transactions from the systems you already run and checks them against that policy all year, so drift surfaces during the year instead of at filing time.

Explore transfer pricing integrations

If value moves between related entities — your parent funding a subsidiary, a sub providing development or support, IP licensed across borders, even routine intercompany cost recharges — then yes, you have intercompany transactions that need an arm’s length basis and an agreement. Two entities is enough to create a TP obligation. The clearest exception is a genuine buy/sell flow with no embedded services or IP, which has limited TP implications initially. We’ll confirm which category your actual flows fall into rather than assume, since cost recharges and informal "funding" between entities almost always carry a TP question even when founders don’t realize it.

The right agreement follows what’s actually moving between the entities. A services agreement covers one entity providing development, support, or back-office work to another, typically on cost-plus (markup applied to the cost base — salaries, rent, operational costs). A distribution agreement covers reselling, where one entity keeps an arm’s-length operator margin and remits the rest. A royalty/licensing agreement covers IP. Many setups need more than one — for example, an Indian dev entity on a services agreement and a royalty arrangement on top, depending on how revenue flows. We map your actual transactions first, then put the right contracts around them rather than starting from a template.

The common pattern is the Indian entity providing development or support to the US entity on a cost-plus services basis, with an intercompany services agreement and benchmarking that sets the markup against comparable Indian service providers. The US side documents the markup as arm’s length; the Indian side needs documentation that satisfies Indian requirements as well, with India tying documentation expectations to transaction value. Indian documentation supports an annual filing cycle that runs separately from US deadlines. We handle both ends together so the position is consistent across the corridor rather than two providers telling slightly different stories.

The markup should reflect what an independent provider doing the same functions, with the same risks, would charge — established through benchmarking against comparable companies in recognized databases, with the tested party positioned within the resulting arm’s length range. We set it from data rather than picking a round number that "feels right," and document why it fits given the functional analysis (who does what, who owns what, who bears which risks). That data-backed basis is what makes the markup defensible at audit — an unsupported markup, however reasonable, is the weakest position in any TP inquiry.

The exposure is meaningful and compounds the longer it runs — undocumented or mispriced intercompany flows can lead to adjustments, double taxation, and penalties in any country examining them, and historical losses or profits in the wrong entity can be hard to unwind. The good news is the position can largely be fixed going forward: we build current documentation and benchmarking, put the right agreements in place, and establish a defensible go-forward basis. Prior years can’t be rewritten, but assessing the historical exposure lets you make informed decisions about whether and where to disclose proactively. Getting the next filing cycle right is the cleanest way to stop the bleed.

Book a 30-minute call. We'll review your current intercompany structure, identify what documentation you need, and show you what Commenda would produce — and how long it would take.

By size

By team

Learn

Tools