GST registration in Singapore is essential for foreign companies to comply with local tax regulations, avoid penalties, and operate efficiently within the Singapore market. This guide outlines the key aspects of GST registration for foreign companies, including eligibility requirements, the registration process, and ongoing compliance.

Why Non-Resident Firms Must Register for GST in Singapore?

Non-resident firms must register for GST in Singapore to avoid significant penalties, blocked sales on online marketplaces, and delays in customs clearance, which could severely disrupt operations. Without GST registration in Singapore, businesses face the risk of financial penalties and operational setbacks.

For non-resident businesses operating in Singapore, GST registration is essential to ensure compliance with the Singapore tax laws and facilitate smooth cross-border transactions. GST registration for non-resident businesses in Singapore is essential for conducting legal trade.

When Does a Foreign Business Need to Register for GST in Singapore? Key Triggers

Foreign businesses must register for GST in Singapore under several scenarios, even without a physical presence. The key triggers for GST registration in Singapore include:

- Supplying Remote Services to Consumers (B2C): Foreign suppliers of remote services (e.g. software, streaming, online training) must register for GST if:

- Annual global turnover exceeds SGD 1 million, and

- B2C supplies of remote services to Singapore exceed SGD 100,000 annually.

- Supplying Low-Value Goods (LVG) to Singapore: Foreign sellers of physical goods valued at SGD 400 or less, delivered via air or post, must register if:

- They exceed the SGD 1 million global turnover, and

- LVG sales to Singapore customers exceed SGD 100,000 annually.

- Acting as a Marketplace Operator or Redeliverer: Foreign marketplace operators and redeliverers may be deemed suppliers and required to register if they facilitate B2C remote services or LVG sales to Singapore, and meet the relevant sales thresholds.

Country-Specific Examples

Below are a few examples that illustrate when foreign businesses must register for GST in Singapore:

- United States: A US-based software company selling subscriptions to Singapore consumers must register under Overseas Vendor Registration (OVR) if it crosses both thresholds.

- China: A Chinese e-commerce seller shipping gadgets under SGD 400 via post to Singapore must register if B2C sales exceed SGD 100,000.

Note: For more detailed information on the process, refer to the Singapore GST registration guide provided by the Government of Singapore to ensure compliance.

Registration Thresholds & Nexus Tests

Non-resident businesses must register for GST if their global turnover exceeds SGD 1 million and they make B2C supplies to Singapore exceeding SGD 100,000 in a 12-month period. The following are a few details to be noted:

- Remote services include digital and non-digital services consumed in Singapore without requiring physical presence.

- Low-value goods are imported goods delivered by air or post to Singapore, valued at SGD 400 or less and not GST-exempt.

- Overseas marketplace operators and redeliverers may be deemed suppliers and liable for GST registration under certain conditions.

Singapore GST Number Format Explained

While looking at GST registration in Singapore, it is important to understand the format of the GST ID number. The GST structure in Singapore adheres to a standardized format. It comprises nine characters in total, beginning with the letter ‘M’, followed by a sequence of eight digits. For example, a typical GST registration number may be represented as M12345678.

In Singapore, common mistakes with GST registration numbers include using the wrong starting letter (not ‘M’), entering fewer or more than eight digits, transposing digits, or adding spaces or special characters. These errors can lead to validation issues and delays in processing.

Is a Local Tax Agent or Fiscal Representative Required?

Non-resident businesses do not always need to appoint a local tax agent or fiscal representative for GST registration in Singapore. However, they may choose to do so for ease of compliance. If appointed, the representative may be held jointly liable for tax obligations. Some jurisdictions may require a bank guarantee or bond to secure tax payments, though this varies by country.

Special Schemes & Simplifications

Various special schemes and simplifications are available to ease GST compliance for certain businesses. These schemes are designed to help businesses manage their GST obligations. Key examples include:

- Import GST Deferment Scheme (IGDS): Defer import GST until your next GST return, easing cash flow during trade.

- Major Exporter Scheme (MES): Suspend GST on non-dutiable imports and zero-GST warehouse removals for qualified exporters.

- Zero-GST Warehouse Scheme: Store imported non-dutiable goods in approved warehouses without upfront GST, with tax applied only upon local removal.

- Approved Contract Manufacturer & Trader (ACMT) Scheme: Tailored for manufacturing/export sectors, this scheme suspends GST on imported goods used in outwards processing.

Step-by-Step: How to Register for GST in Singapore?

GST (Goods and Services Tax) is a consumption tax applied to most goods and services sold in Singapore. To register for GST in Singapore, follow these steps:

- Identify whether your registration is compulsory (e.g., taxable turnover > SGD 1 million) or voluntary.

- For voluntary registration, key business personnel (e.g., director, preparer) must complete the “Overview of GST” e-learning and quiz, unless exempt due to experience or credentials.

- Ensure you’re authorized via Corppass for the digital service “GST (Filing and Application)” and have all required documents ready in softcopy.

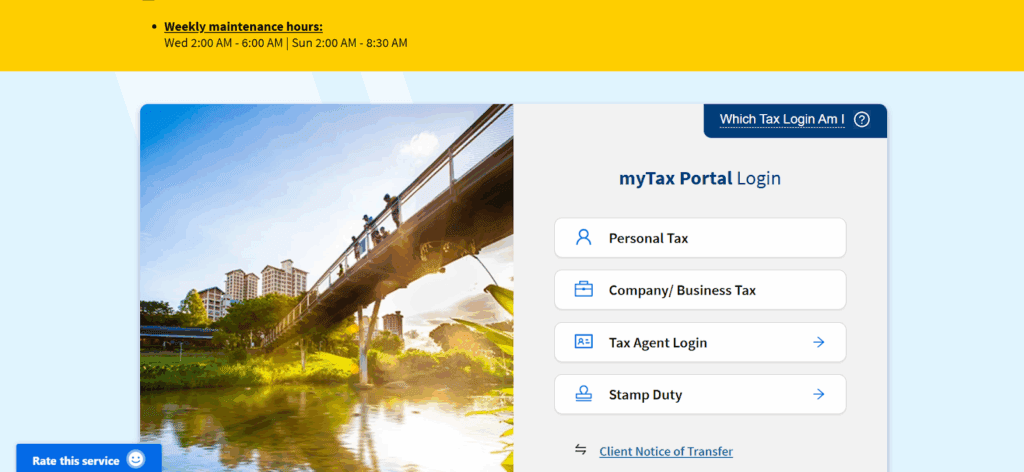

- Access myTax Portal and submit your GST registration with supporting documents.

Note: For overseas vendors, submit via the OVR registration form.

- Inland Revenue Authority of Singapore (IRAS) processes 60% of applications within 10 working days, others within 30 days. If successful, IRAS will notify you by post, email, or SMS.

Required Documents Checklist

When registering for GST in Singapore, you will need to provide several key documents to complete your application. Below is a checklist of the required documents you should gather before starting the registration process:

- Business Registration Proof: Latest ACRA BizFile (or equivalent incorporation documents for non-UEN entities).

- Proof of Identity & Appointment (for overseas entities): Valid passport or ID of director/trustee, plus signed letter appointing a local agent.

- Evidence of Business Activity: Invoices or revenue statements for the past two months.

- GIRO Application Form: Required for voluntary registrants to facilitate GST payments and refunds; submit via eGIRO or mail to IRAS.

- e-Learning Acknowledgement: Voluntary GST applicants must provide proof of completion & quiz for the “Overview of GST” e-learning.

Processing Time & Government Fees

When you register for GST online in Singapore via the myTax Portal, processing typically takes up to 10 working days, though it may take up to 30 days if additional documents or checks are required. GST registration is effective from the date stated in the IRAS approval letter, not the date of application.

There is no registration fee, but businesses may incur costs if they engage professional tax or accounting services.

Post-Registration Obligations

After your GST registration in Singapore, there are several ongoing obligations to ensure compliance with the IRAS. These include reporting, record-keeping, and paying GST collected from your customers. Below are the key post-registration obligations:

- Filing frequency & deadlines: GST returns must be filed via myTax Portal approximately monthly or quarterly. The regular GST return is Form F5. A final return (F8) must be submitted upon deregistration to account for GST up to the last day of registration.

- Payment due dates & penalties: GST payments are due by the filing due date. GIRO payments are taken on the 15th of the following month. Late payments incur a 5% penalty, plus 2% monthly interest (capped at 50%). Late filing incurs flat penalties starting at S$200/month, up to S$10,000.

- e‑Invoicing (InvoiceNow): From May 2025, businesses can voluntarily adopt InvoiceNow for structured e‑invoice transmission.

- Record‑keeping requirements: Maintain invoices, accounting records, bank statements, ledgers, and supporting documents for at least 5 years in either paper or electronic form.

Claiming Input-Tax Credits & Refunds as a Non-Resident

Non-resident businesses can claim GST refunds on business expenses incurred in Singapore. To do so, they must meet certain criteria and follow specific procedures. Here are the conditions:

- Automatic Refunds within 30 Days: IRAS automatically refunds GST credits and pays interest if not refunded within 30 days from the date the tax credit arises, except where refunds are ineligible. This includes businesses with non-resident tax registration in Singapore.

- Eligibility Criteria: Non-residents (including businesses or departing individuals) must maintain a local Singapore bank account and register for GIRO or PayNow Corporate linked to their UEN to receive refunds.

- Exceptions to Automatic Refunds: Refunds under S$15 or those retained for future offsets will not be automatically returned.

Penalties for Late Registration or Non-Compliance

If a business fails to comply with GST registration or submission deadlines, then the IRAS imposes various penalties and interest charges. Here’s a concise overview of the consequences of late registration or non-compliance:

- Late GST Registration: A fine of up to SGD 10,000 and a 10% penalty on the GST due. IRAS may backdate the registration to when liability first arose.

- Late Filing of GST Returns: An immediate SGD 200 penalty, plus SGD 200 for every full month the return remains outstanding (capped at SGD 10,000 per return).

- Late GST Payment: A 5% late payment penalty is imposed on the unpaid tax. An additional 2% per month penalty applies after 60 days, up to a maximum of 50% of the tax due.

Deregistration & GST Number Changes

When your business no longer needs to be GST-registered or if there are changes to your GST number, there are certain conditions and processes to be followed. The following are the details:

- Mandatory Deregistration: Apply within 30 days if your business ceases, stops taxable supplies, changes legal entity, or is fully transferred.

- Voluntary Deregistration: Allowed if not liable, but only after 2 years of voluntary registration.

- Application: Submit online via myTax Portal; most are processed on the same day.

- Final Return: File GST F8 for the last period, accounting for GST on business assets (if value > SGD 10,000) and unbilled supplies before deregistration.

Conclusion

Understanding GST registration in Singapore is essential for any foreign business operating here. Whether you need to register due to exceeding the GST threshold, voluntarily register, or update/cancel your GST registration, meeting deadlines and adhering to regulations are key to avoiding penalties.

GST registration can be complex for foreign companies, but Commenda can help. Our experienced team specializes in assisting foreign businesses with GST registration and compliance with IRAS guidelines.

Focus on growing your business in Singapore, while we handle your GST obligations. Book a free demo with Commenda today to see how we can help!