As a business owner, understanding the differences between 1099-NEC and 1099-MISC forms is crucial for accurate tax reporting. Both forms are used to report income, but they serve different purposes under IRS guidelines. The 1099-NEC is specifically used to report non-employee compensation. However, the 1099-MISC is used for various other types of income, including rents, prizes, and other miscellaneous payments.

In this article, we will explain the key differences between 1099-NEC vs 1099-MISC. We will also show you when to use each form and the impact on both businesses and recipients.

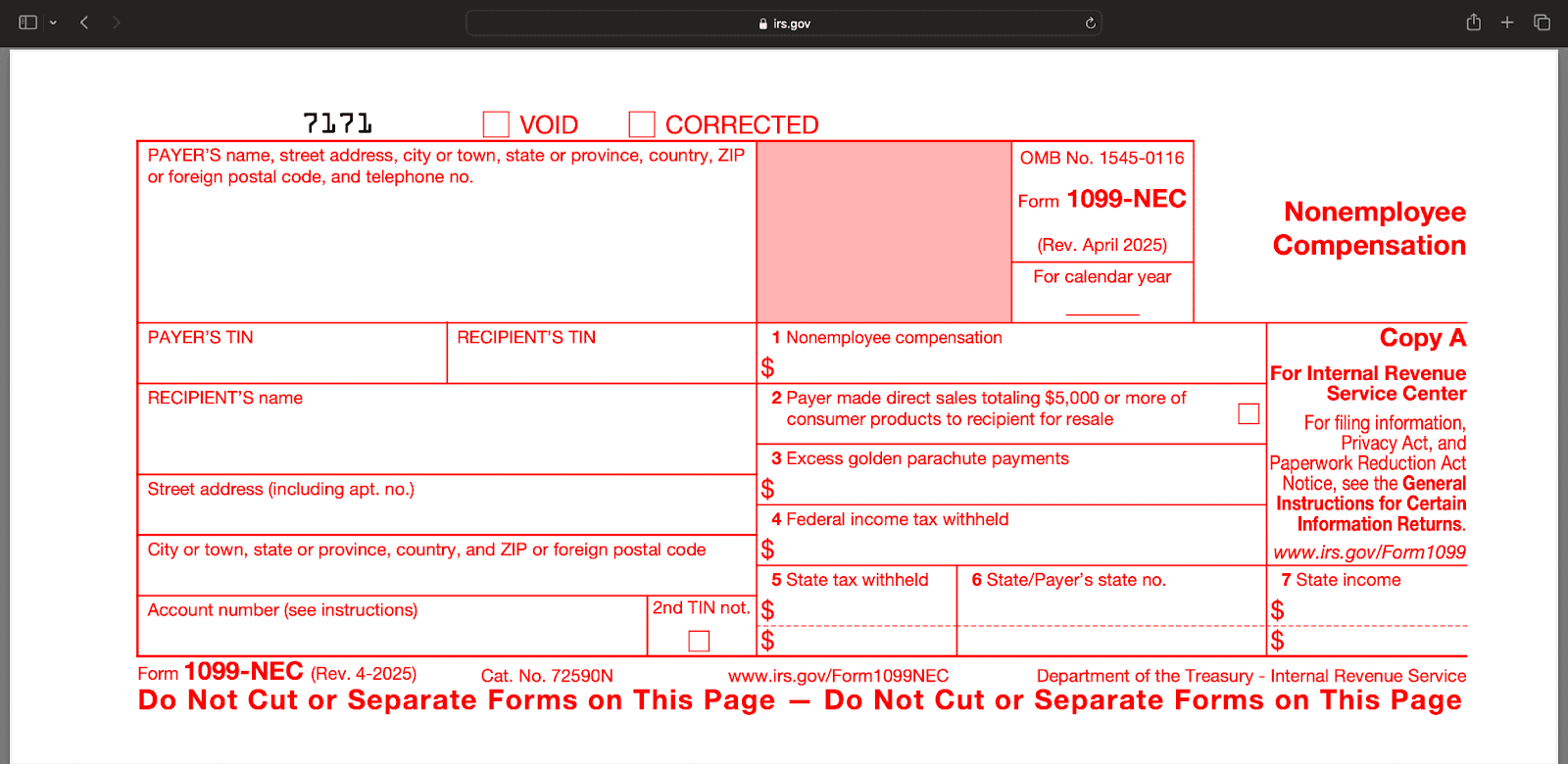

What is Form 1099-NEC?

The 1099-NEC form is used primarily to report non-employee compensation. If your business has paid $600 or more to a contractor or freelancer for services, you’ll likely need to issue a 1099-NEC.

The 1099-NEC specifically focuses on payments made to individuals who are not employees of the company. For more information on Form 1099-NEC, click here.

Filing Requirements

- Threshold: Payments must exceed $600 to require reporting on Form 1099-NEC.

- Deadline: Must be filed with the IRS and sent to recipients by January 31.

- Information Required: Includes the business’s and recipient’s details, such as names, addresses, and tax identification numbers.

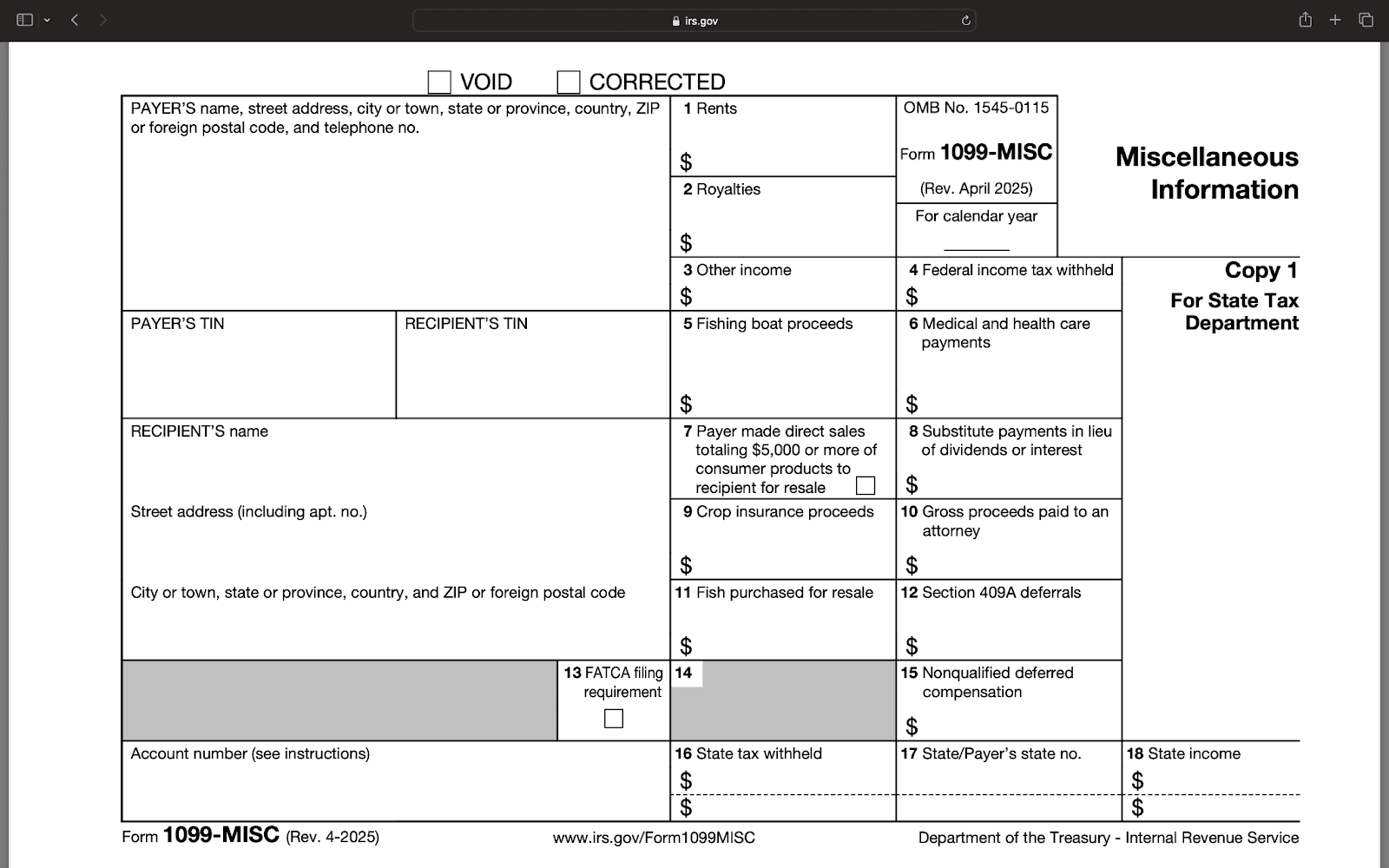

What is 1099-MISC?

Form 1099-MISC reports miscellaneous income not related to nonemployee compensation. This includes rent payments, royalties, prizes and awards, medical and healthcare payments, and attorney fees (excluding legal settlements). For more information on Form 1099-MISC, click here.

Filing Requirements

- Thresholds: Vary by type of payment:

- Rent: $600 or more.

- Royalties: $10 or more.

- Prizes and Awards: $600 or more.

- Deadline: Must be sent to recipients by January 31 and filed with the IRS by February 28 (paper) or March 31 (electronic).

Now that you have understood the difference between the two forms let’s understand some details on the changes and reintroduction of Form 1099-NEC.

Changes and Reintroduction of Form 1099-NEC

In 2020, the IRS reintroduced Form 1099-NEC to provide better clarity and reduce confusion in reporting non-employee compensation.

Prior to this change, businesses reported non-employee compensation, such as payments to independent contractors, freelancers, and consultants, on Form 1099-MISC, specifically in Box 7. This box, however, also included other types of income, like rents and legal settlements, leading to complications and errors during tax filing.

To simplify the process and ensure accurate reporting, the IRS separated non-employee compensation from other income types by creating the 1099-NEC.

This form is now exclusively used to report payments of $600 or more to independent contractors and other non-employee service providers. This change makes the filing process easier for both businesses and contractors.

1099-NEC vs 1099-MISC: Key Differences Explained

When reporting income to the IRS, businesses must decide whether to use Form 1099-NEC or Form 1099-MISC. Both forms report different types of payments, but it’s important to know when to use each.

Let’s break down the key differences:

1. Purpose

- Form 1099-NEC: This form is used explicitly for reporting non-employee compensation. If you paid $600 or more to an independent contractor or freelancer for services they provided, you’ll report it here.

- Form 1099-MISC: This form covers a broader range of payments. It’s used to report payments such as rent, royalties, prizes, and other types of miscellaneous income.

2. Payment Thresholds

- Form 1099-NEC: Requires reporting for payments of $600 or more to nonemployees for services rendered.

- Form 1099-MISC: Thresholds vary by payment type:

- Rent: $600 or more.

- Royalties: $10 or more.

- Prizes and Awards: $600 or more.

3. Types of Payments Reported

- Form 1099-NEC:

- Non-employee compensation (payments to independent contractors, freelancers, consultants, etc.).

- Form 1099-MISC:

- Rents.

- Royalties.

- Other income (e.g., awards or prizes).

- Medical payments.

- Payments to attorneys, and more.

4. Filing Deadlines

- Form 1099-NEC: You need to file this form by January 31st. This is the same date as for W-2 forms, so it’s an important deadline for employers to remember.

- Form 1099-MISC: The deadline to file this form is February 28th if filed on paper or March 31st if filed electronically.

5. Tax Implications

- Form 1099-NEC: Payments are subject to self-employment tax for recipients4.

- Form 1099-MISC: Payments are generally not subject to self-employment tax but are still taxable income4.

6. Box Numbers on the Forms

- Form 1099-NEC:

- Box 1: Non-employee compensation.

- Form 1099-MISC:

- Box 1: Rents.

- Box 2: Royalties.

- Box 3: Other income (e.g., prizes, awards).

- Box 6: Medical and healthcare payments.

- Box 10: Payments to attorneys.

Consequences of Non-Compliance and Strategies for Success

Meeting the filing deadlines for Forms 1099-NEC and 1099-MISC is essential to avoid costly penalties and practice prevention strategies:

Penalties

- Avoid Late Filing Penalties: The IRS imposes penalties for late filing:

- $50 per form if filed within 30 days.

- $110 per form if filed 31 to 180 days late.

- $270 per form if filed more than 180 days late.

- These penalties can quickly add up, especially if filing many forms.

- Failure to Furnish Penalties: If you fail to send forms to recipients by January 31st, you face penalties of:

- $50 per form within 30 days.

- $110 per form for 31 to 180 days.

- $270 per form after 180 days.

Prevention Strategies

- Accurate Record Keeping: Maintain detailed records of all payments to ensure accurate reporting.

- Timely Communication: Ensure timely filing to help contractors and vendors meet their tax obligations, fostering strong business relationships through reliable communication.

- Consult Professionals: Consider hiring a tax professional to ensure compliance with IRS regulations.

- Demonstrate Reliability: Prioritize timely and accurate filing to project a reliable and trustworthy business image, safeguarding your reputation and maintaining stakeholder confidence.

- Establish Processes: Set up a system to meet deadlines consistently, preventing the need for costly corrections and minimizing administrative burdens.

Don’t let tax filing penalties get in the way of your success. With Commenda, you can automate your 1099-NEC and 1099-MISC filings, ensuring timely and accurate submissions

Guidelines for Issuers of Forms 1099-NEC and 1099-MISC

Issuers of Forms 1099-NEC and 1099-MISC must follow specific guidelines to ensure compliance with IRS requirements. Here’s a breakdown of the key points:

1. 1099-NEC vs 1099-MISC: Understanding Who Receives Each Form

- Form 1099-NEC: This form is issued to independent contractors, freelancers, and sole proprietors. It reports nonemployee compensation for services rendered. You must file a 1099-NEC if you’ve paid $600 or more to these individuals or businesses during the tax year.

- Form 1099-MISC: Issued for miscellaneous payments not related to nonemployee compensation, such as rent, royalties, prizes, medical or healthcare payments, or other types of income.

2. Get the Correct Information from Recipients

When filing a 1099-NEC vs 1099-MISC form, you need to collect accurate information from recipients. This can be done by having them complete Form W-9, which includes:

- Name or business name

- Taxpayer Identification Number (TIN) or Social Security Number (SSN)

- Address

3. Filing Methods

- Paper Filing: If filing fewer than 250 forms, you can file paper forms with the IRS.

- Electronic Filing: If filing 250 or more forms, you must file electronically using the IRS e-file system.

4. Filing Deadlines

- Form 1099-NEC: Must be filed with the IRS by January 31st. You must also send it to the recipient by this date.

- Form 1099-MISC: If filing on paper, the deadline is February 28th. If filing electronically, the deadline is March 31st. Recipients must receive the form by January 31st.

Note: Filing electronically can simplify the process and help avoid mistakes.

5. State Filing Requirements

In addition to IRS filings, many states have their own filing requirements for Form 1099. Some states require separate submissions, while others accept federal filings. Make sure to check the requirements for the states in which you operate.

6. Backup Withholding Requirements

If you are aware that a payee’s TIN is incorrect, you must withhold federal income tax at a rate of 24% (backup withholding). You must also submit the withheld amount to the IRS along with your 1099 filings.

7. Amending Forms

If you find an error after filing, you must file an amended form. Use Form 1099-NEC or 1099-MISC to correct any mistakes and submit it to the IRS. Be sure also to send the corrected form to the recipient.

8. Maintaining Records

As an issuer, you are required to keep records of your filings for at least three years. These records should include:

- A copy of each 1099 form filed

- Supporting documentation (for example, Form W-9 from recipients)

- Any correspondence related to 1099 filings

State Requirements and Compliance for Form 1099-NEC and Form 1099-MISC

Many states have their own 1099 filing requirements, in addition to federal guidelines. States like California, New York, and Virginia require separate filings, so check state-specific instructions.

Some states mandate electronic or paper filing, and may have their own forms, deadlines, and tax rules. Certain states also require withholding on non-employee compensation or additional reporting, such as payment breakdowns.

Non-compliance may result in late fees and interest charges. Stay compliant by regularly checking state tax agency websites and using e-filing when available.

Staying on top of 1099 filings can be challenging, but Commenda makes it easier. With automated tools and expert support, Commenda helps ensure your forms are filed accurately and on time, avoiding penalties and compliance issues.

Best Practices for Filing Form 1099-NEC and Form 1099-MISC

Here are the best practices to follow when preparing and filing your 1099-NEC and 1099-MISC forms:

- Start Early and Collect W-9 Forms Promptly: Request W-9 forms from vendors at the beginning of your working relationship to avoid last-minute scrambles for information.

- Stay Organized Throughout the Year: Use tools like Commenda to maintain accurate records and create a centralized system for storing W-9s, invoices, and contracts.

- Consider Electronic Filing: For large volumes of 1099 forms, e-filing is faster, more accurate, and reduces the risk of penalties.

- Know the Deadlines: Ensure timely filing by remembering that Form 1099-NEC must be filed by January 31, and Form 1099-MISC has different deadlines for recipients and the IRS.

- Maintain Accurate Records: Keep detailed records of all filings for at least three years, including copies of 1099 forms and supporting documentation.

- Consult Professionals: Consider consulting a tax professional if you are unsure about any aspect of the 1099 filing process or have complex tax situations.

Conclusion

Filing 1099-NEC vs 1099-MISC forms may seem like a tedious task, but it’s essential for staying compliant with IRS regulations and avoiding costly penalties. With Commenda, you need not worry about the right systems and processes in place, and 1099 filing doesn’t have to be stressful.

Don’t let sales tax complexities hold your business back. Partner with Commenda for expert guidance. Schedule a free call with our sales tax experts today!