In an increasingly globalized economy, U.S. taxpayers who own foreign corporations must navigate complex tax regulations. One of the most critical forms they need to be aware of is Form 5471. This form is not just a bureaucratic requirement; it plays a crucial role in ensuring compliance with U.S. tax laws regarding foreign income and ownership. Understanding who needs to file, the requirements involved, and the potential penalties for non-compliance is essential for any U.S. owner of a foreign corporation.

What Is Form 5471 and What Is It Used For?

What Is a 5471 Form Used For? IRS Compliance for Foreign Corporation Ownership

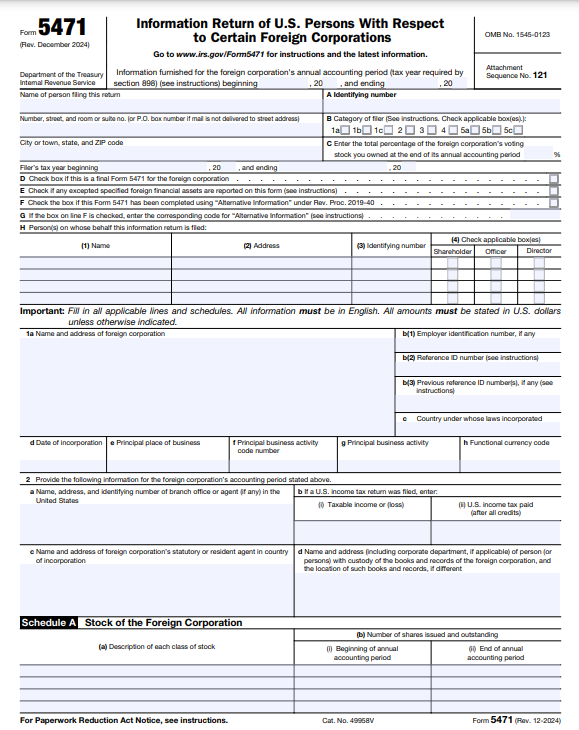

Form 5471 is an informational return that U.S. citizens and residents must file if they are officers, directors, or shareholders in certain foreign corporations.

This form provides the IRS with information about the foreign corporation’s activities, financial status, and ownership structure. It helps ensure that U.S. taxpayers are accurately reporting their foreign income and complying with international tax laws.

For instance, the form requires detailed reporting on income statements, balance sheets, and related-party transactions, offering a comprehensive view of the foreign entity’s financial health.

5471 Filing Requirement: When and Why the Form Is Necessary

Filing Form 5471 is necessary when specific ownership thresholds are met. Generally, if a U.S. person owns at least 10% of a foreign corporation’s stock, they must file this form.

The requirement exists to prevent tax evasion through offshore entities and to ensure that U.S. taxpayers report their worldwide income.

Without this requirement, it would be significantly easier for individuals and corporations to hide income offshore and avoid paying U.S. taxes.

How Form 5471 Relates to CFCs (Controlled Foreign Corporations) and Foreign Tax Credits

Form 5471 is particularly relevant for Controlled Foreign Corporations (CFCs). A CFC is defined as a foreign corporation where U.S. shareholders own more than 50% of the total combined voting power or value of the stock. Filing Form 5471 allows U.S. shareholders to claim foreign tax credits, which can offset their U.S. tax liabilities on income earned abroad. For example, if a U.S. company owns 60% of a CFC and the CFC pays foreign income taxes, the U.S. company can use those foreign tax payments to reduce its U.S. tax liability, preventing double taxation.

First-Time Filers: Ensuring Historical Data Is Accurate

For first-time filers, it’s crucial to gather historical data accurately to report on Form 5471 effectively. This includes understanding the corporation’s financial history and ownership changes over time to ensure compliance with IRS requirements. Gathering this data can be a complex process, particularly if the foreign corporation has not maintained detailed records or has undergone significant changes in ownership or structure.

Foreign Corporation’s Tax Year vs. U.S. Tax Year: How to Handle It?

When dealing with foreign corporations, it’s essential to align their tax year with that of the U.S. taxpayer’s reporting year If there’s a discrepancy, filers may need to make adjustments or report on a different basis to maintain compliance. This often involves converting financial data from the foreign corporation’s fiscal year to the U.S. taxpayer’s reporting year, which may require additional accounting work and currency conversions.

Once You File, Do You Have to Keep Filing?

Yes, once you file Form 5471 for a particular foreign corporation, you generally have an ongoing obligation to file it annually as long as you meet the ownership requirements.

Who Needs To File Form 5471?

5471 Categories: Understanding Categories 1–5 for Different Filers

Form 5471 has five categories of filers based on ownership percentages and roles within the corporation:

- Category 1: U.S. citizens or residents who are officers or directors of a foreign corporation. This category ensures that individuals with significant control over the foreign corporation are reporting its activities to the IRS.

- Category 2: U.S. shareholders who own at least 10% of the stock. This category captures individuals who have a substantial financial interest in the foreign corporation.

- Category 3: U.S. shareholders who own at least 10% of a CFC. This category focuses on U.S. shareholders who have a significant interest in a controlled foreign corporation.

- Category 4: U.S. persons who acquire stock in a foreign corporation. This category captures individuals who have recently invested in a foreign corporation.

- Category 5: Any U.S. person who owns shares in certain foreign corporations. This is a broad category that captures various types of U.S. shareholders in foreign corporations.

Form 5471 Eligibility Criteria: Who Qualifies?

Eligibility criteria vary by category but generally focus on ownership percentages and roles within the corporation. For example, a Category 1 filer must be a U.S. citizen or resident who serves as an officer or director of a foreign corporation, regardless of their ownership percentage. In contrast, a Category 2 filer must own at least 10% of the foreign corporation’s stock.

Does a Partnership File Form 5471? When Partnerships or LLCs Need to File

Partnerships may need to file Form 5471 if they have partners who meet the filing requirements based on their ownership stakes in a foreign corporation. For example, if a U.S. partnership owns 15% of a foreign corporation, the partners may be required to file Form 5471 depending on their ownership stakes in the partnership.

Do I Have to File Form 5471 Every Year? Annual Filing Obligations and Exemptions

If you continue to meet the filing requirements, you must file Form 5471 annually unless specific exemptions apply. Some exemptions may apply if the foreign corporation is dormant or if the U.S. shareholder meets certain de minimis requirements.

Form 5471 Filed on Behalf Statement: When Someone Else Can File on Your Behalf

In certain situations, another party can file Form 5471 on your behalf if they have been authorized by you to do so This might occur if the U.S. shareholder is incapacitated or if a designated representative has been authorized to handle their tax filings.

What Is the Difference Between Form 5471 and Form 5472?

5471 vs. 5472: Who Files Which Form and for What Reason?

While both forms serve informational purposes related to foreign entities, Form 5472 is specifically for foreign-owned U.S. corporations, whereas Form 5471 pertains to U.S. shareholders of foreign corporations. Understanding this distinction is critical to ensure that the correct form is filed.

Common Filing Mistakes Between the Two Forms

Common mistakes include misclassifying entities or failing to provide complete information on related party transactions. For example, a U.S. subsidiary of a foreign corporation might incorrectly file Form 5471 instead of Form 5472, or vice versa. Another common mistake is failing to disclose all related-party transactions, which can trigger additional scrutiny from the IRS.

When Is Form 5471 Required to Be Filed?

Standard Filing Deadlines: Individuals and C Corporations

The standard deadline for filing Form 5471 is typically aligned with your annual tax return due date (April 15 for individuals; March 15 for corporations).

S Corporations and Partnerships

S Corporations and partnerships also follow similar deadlines but should be aware of specific rules regarding extensions.

Fiscal Year Filing Rules

If your business operates on a fiscal year rather than a calendar year, different rules may apply regarding when you must file.

5471 Instruction for Late Filing: Extensions and Reasonable Cause Exceptions

If you miss the deadline, you may apply for an extension or demonstrate reasonable cause for late filing to avoid penalties. Reasonable cause might include situations such as a natural disaster or a serious illness that prevented the taxpayer from filing on time.

Step-by-Step Process to File Form 5471 Instructions Accurately

Filing Form 5471 involves several steps:

Step 1 – Identify Your Filing Category

Determine your category based on ownership percentage and role within the corporation. This is the first and most critical step, as it determines which parts of the form you need to complete and which schedules are required.

Step 2 – Gather Required Information

Collect necessary details such as (but not limited to)

- Foreign Corporation Name: The legal name under which the corporation operates.

- Employer Identification Number (EIN): The unique identifier assigned by the IRS.

- Country of Incorporation: Where the company is legally registered.

- Shareholder Details: Including Tax Identification Number (TIN) and ownership percentage.

- Financial Statements: These should include balance sheets and income statements from previous years

Step 3 – Complete the Required Form 5471 Schedules

Each schedule serves specific reporting purposes:

- Main Form: Basic company information.

- Schedule A: Stock structure.

- Schedule B: List of U.S. shareholders.

- Schedule C: Income statement in USD.

- Schedule F: Balance sheet.

- Schedule E: Foreign taxes paid.

- Schedule G: Other information related to Subpart F.

- Schedule H: Current earnings and profits.

- Schedule I: Shareholder’s income from the foreign corporation.

- Schedule J: Accumulated earnings.

- Schedule M: Related-party transactions.

- Schedule O: Changes in corporate structure.

Step 4 – Submit Form 5471 with Your U.S. Tax Return

You can e-file if allowed; otherwise, submit it alongside your tax return.

Understanding IRS Penalties: What Happens If I Fail to File Form 5471?

Failure to file can result in significant penalties:

Monetary Penalties

The IRS imposes substantial fines for late or non-filing, which can accumulate over time. The initial penalty can be up to $10,000 per form per year for failure to timely file or furnish required information. If you fail to file after receiving a notice from the IRS requesting compliance, additional penalties may apply, potentially increasing up to $50,000 per form per year.

Impact on Foreign Tax Credits

Not filing may also affect your ability to claim foreign tax credits which can lead to double taxation on income earned abroad—an issue that significantly impacts profitability for businesses operating internationally.

Effect on IRS Audits & Statute of Limitations

Failure to comply can lead to increased scrutiny from the IRS during audits; moreover, not filing could potentially extend the statute of limitations indefinitely until all required returns are filed.

Increased IRS Scrutiny

Non-compliance may trigger further investigations into your financial activities; this could lead not only towards additional audits but also create complications in other areas such as personal finances or future business dealings due diligence processes.

Criminal Penalties for Willful Evasion

In severe cases where willful failure occurs—such as knowingly disregarding reporting obligations—criminal charges could be brought against individuals involved which may result in hefty fines or even imprisonment depending upon severity.

IRS Late-Filing Relief Programs

The IRS offers relief programs like Streamlined Filing Compliance Procedures for those who missed deadlines but wish to rectify their filings without severe penalties. These programs are designed specifically for taxpayers who may not have been aware of their obligations or those living outside the United States during relevant periods; eligibility criteria vary depending upon individual circumstances but often include:

- Proof that non-compliance was not willful

- Evidence showing efforts made towards compliance once awareness was established

- Timely submission post-discovery

What To Do If You Miss The Deadline? Filing Extensions & IRS Notifications

If you miss your deadline, notify the IRS immediately through appropriate channels, this could involve submitting an extension request along with any necessary documentation explaining circumstances surrounding missed deadlines. Exploring available options for extensions or corrections should be prioritized as soon as possible since proactive measures often mitigate potential penalties significantly compared to autoreactive responses later down the line.

Avoid These Common Mistakes When Filing Form 5471

To ensure compliance while avoiding pitfalls associated with this complex process consider these common errors:

- Misclassifying your filing category based upon incorrect assumptions about ownership percentages

- Incomplete stock ownership details leading to inaccurate representations within submitted forms

- Currency translation errors resulting from miscalculating values due to discrepancies between local currencies versus USD equivalents

- Overlooking related-party transactions which could trigger additional scrutiny if not properly disclosed

- Miscalculating earnings/profits figures causing discrepancies between reported amounts versus actual performance metrics

- Misunderstanding Subpart F rules leading towards improper classifications affecting overall taxation strategies

- Failing when dealing with dormant entities thereby missing opportunities available under current regulations

What Is the Average Fee for Form 5471?

The cost of preparing Form 5471 can vary widely based on complexity but typically ranges from $500 up to $2,500 when hiring professional assistance—this variance often depends upon factors such as:

- Size/structure complexity associated with the entity being reported upon

- Volume/quality required documentation needed during the preparation phase

- Expertise level possessed by the preparer handling the submission process itself

Some Key Takeaways For Successful Reporting

To ensure successful reporting consider these key takeaways:

- Follow IRS instructions carefully; always reference official guidelines provided directly to them whenever possible.

- Stay compliant with all deadlines established; utilize calendar reminders/alerts if necessary.

- Consider hiring professionals if complexities arise, don’t hesitate to seek help when needed.

Conclusion

Navigating complexities of international taxation requires diligence in understanding forms like Form 5471; By staying informed about filing requirements/deadlines/penalties/best practices owners can ensure compliance while minimizing risks associated with non-filing inaccuracies reporting. As regulations evolve continuous education will be key to maintaining adherence to both domestic/international obligations.

For further insights into managing your taxes efficiently or exploring more resources related to business finances/compliance, reach out to us at Commenda, and stay informed as regulations evolve each year.

FAQs On Form 5471

-

How does Form 5471 relate to international information returns?

Form 5471 complements other forms like the FinCEN Report (FBAR) by providing detailed information about foreign entities owned by U.S. taxpayers; understanding how each interaction helps a comprehensive picture ensuring full compliance across the board.

-

Can I electronically submit my returns?

Yes. E-filing is allowed under certain conditions, consult IRS guidelines specifics regarding eligibility requirements before proceeding.

-

What happens if I fail to submit previous years’ filings?

You should rectify past filings ASAP utilizing available relief programs offered by the IRS designed specifically to assist those facing challenges meeting obligations.

-

How do I report multiple foreign corporations?

Complete separate Forms 5471 for each owned unless specific conditions allow otherwise—maintaining clear records simplifies this process immensely.

-

What records should I keep supporting filings?

Maintain detailed records including financial statements/ownership documents/correspondence-related filings—organization key during audits.

-

Can Form 5471 be filed separately from the primary return?

No. Must be submitted alongside primary tax return (e.g., Forms1040 or1120)—ensure everything is filed together appropriately.

-

How often does the IRS update instructions?

Typically updates annually however mid-year updates may occur based on legislative changes/new regulations affecting processes overall.

-

What records should kept audits audit-related filings?

Keep all relevant documents organized/accessible in case an audit arises—this includes financial statements/correspondence regarding submissions.