All companies incorporated in Singapore must file their estimated chargeable income every year. This blog post explains the ECI filing and walks you through the filing process, eligibility requirements, deadlines, and potential benefits.

What is the Estimated Chargeable Income (ECI) in Singapore?

ECI is an estimate of a company’s taxable income for a particular assessment year. The Inland Revenue Authority of Singapore (IRAS) uses this information for tax planning purposes and to assess a company’s potential tax liability.

Who needs to file ECI?

Every company incorporated in Singapore is required to file an ECI within three months from the end of its financial year. However, there are a few exceptions:

Additional ECI Waiver Eligibility: Companies without ECI for a particular financial year are also eligible for an ECI waiver, provided the income is calculated before deducting any tax exemptions. ECI Exemptions:

- Companies with an annual revenue of S$5 million or below qualify for an ECI filing waiver, provided they did not have any ECI for that financial year.

- Companies without ECI for a particular financial year are also eligible for an ECI waiver, provided the income is calculated before deducting any tax exemptions. ECI Exemptions:

- Certain companies with special circumstances might be exempt from ECI filing. These include:

- Foreign ship owners or charterers whose local shipping agent has submitted/ will submit the Shipping Return

- Foreign universities

- Designated unit trusts and approved CPF unit trusts

- Real estate investment trusts that have been granted the tax treatment

- Cases specifically granted the waiver to furnish ECI by IRAS

Benefits of on-time ECI filing in Singapore

Aside from staying compliant with IRAS, the ECI offers some benefits:

- Avoids estimated assessments: If you fail to file your company’s ECI on time, IRAS might issue an estimated Notice of Assessment (NOA) based on their calculations. This could potentially lead to a higher tax bill than your actual liability.

- Enables early tax planning: Knowing your estimated tax liability through ECI filing allows for better tax planning and budgeting throughout the year.

- Improves compliance reputation: Timely ECI filing demonstrates good corporate governance and adherence to tax regulations.

The ECI filing process

The ECI filing process in Singapore is generally straightforward and can be completed online via the IRAS myTax Portal:

- Log in to myTax Portal: Access the IRAS myTax Portal using your SingPass or CorpPass. Click here to access the portal

- Ensure your business user is authorized as an “Approver”: Either you or the representative has to be given authorization from the company to be eligible for filing your company’s ECI.

- Navigate to the ECI filing: Locate the “Corporate Tax” section and select “File ECI.”

- Prepare necessary information: Gather relevant financial data for your company, including income, expenses, deductions, and tax allowances.

- Complete the ECI form: The online ECI form will guide you through entering the necessary information. You can save your progress and return later if needed.

- Submit and acknowledge: Once you’ve reviewed and confirmed the details, submit your ECI filing electronically. You’ll receive an acknowledgment from IRAS upon successful submission.

Important Note: Non-resident companies or those without a local presence in Singapore might require a local filing agent to facilitate the ECI filing process.

Documents required for the ECI filing

When preparing the documents for completing the Estimated Chargeable Income (ECI) forms, make sure you have the following:

- SingPass or CorpPass

- company’s Unique Entity Number (UEN)

- CorpPass login details

- Necessary accounting records (e.g. financial statements, revenue and expense details, supporting documents, and any other relevant financial information needed)

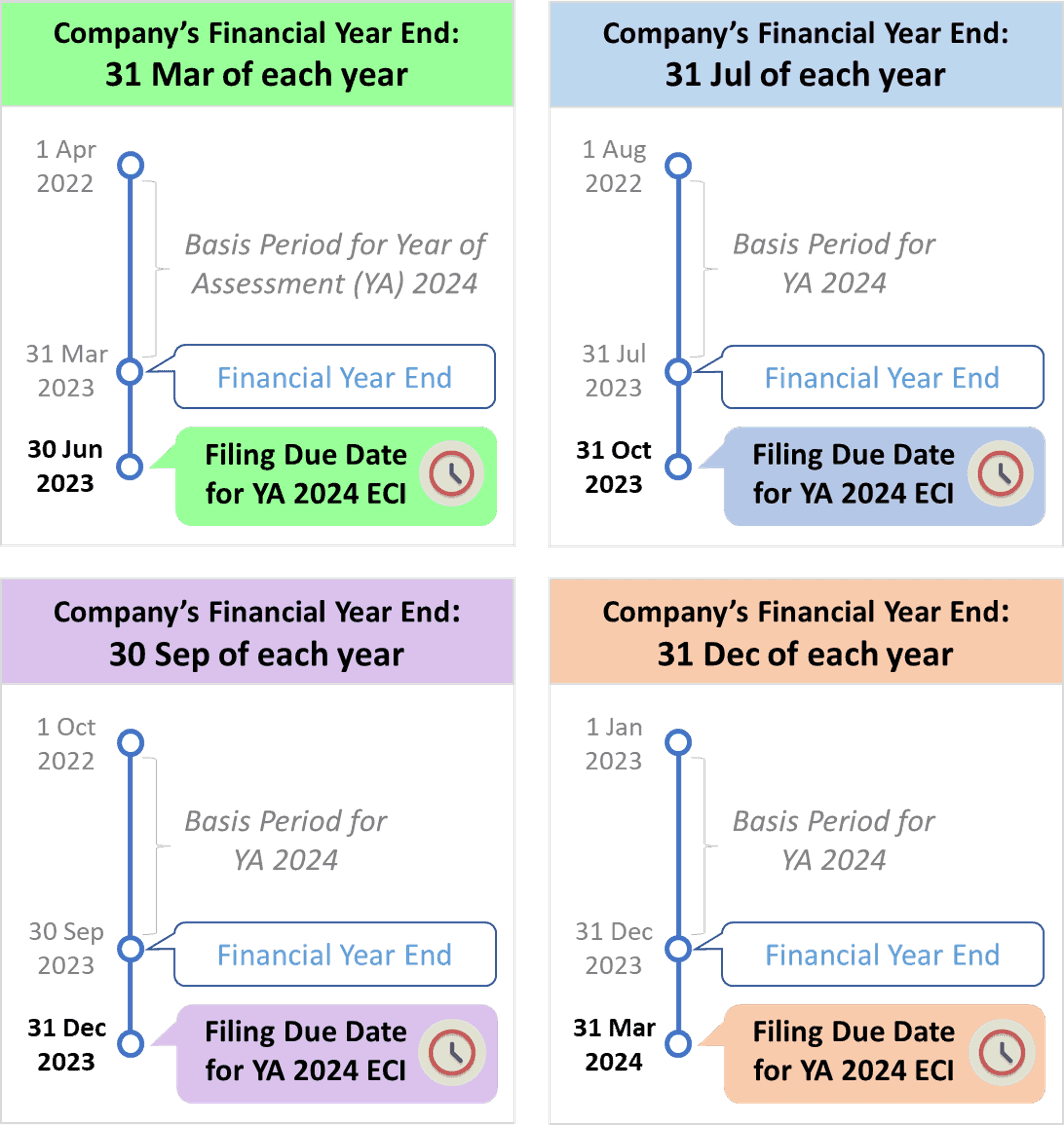

When is ECI due?

You need to file ECI within 3 months from the end of your company’s financial year.

Your company should receive a notification from the Inland Revenue Authority of Singapore (IRAS) to file its ECI during the last month of its financial year.

If your company did not receive the notification and is not eligible for ECI filing exemption, it is still required to file its ECI within 3 months from the end of its financial year.

Examples of ECI filing due dates for different financial year ends:

What happens if my company fails to file its ECI?

If your company is required to file its ECI but fails to do it within 3 months from the end of its financial year, you might receive a notice of assessment that may be issued based on an estimation of your company’s income.

How to pay the estimated tax after ECI filing?

Once the Inland Revenue Authority of Singapore (IRAS) has processed your company’s ECI filing, you can access the Notice of Assessment through the mytax.iras.gov.sg/ESVWeb/default.aspx portal.

The Notice of Assessment serves as an official document that outlines the amount of tax your company is required to pay.

Please note that if your company files a nil ECI, no Notice of Assessment will be issued.

Your company must pay the tax payable amount within 1 month from the date of the Notice of Assessment – unless you qualify for installments.

You pay the estimated tax through 2 methods:

- Payment through GIRO: Singapore-registered companies can sign up for GIRO to pay estimated tax in installments. Click here

- Electronic Payment: You can also make payments through Internet Banking, Phone Banking, or NETS. View details on all electronic payment modes.

What happens if my company’s ECI filing is late or disqualified?

If you miss the Estimated Chargeable Income (ECI) submission deadline, you will receive a Notice of Assessment (NOA) Type 2.

Should your company disagree with the estimated tax assessment, follow these steps: File an objection within two months of receiving the NOA.

Provide reasons for late or non-filing of ECI and propose a revised ECI amount in your objection. Regardless of the objection’s outcome, pay the full amount stated in the NOA within 1 month of its issuance.

If your objection is successful and results in an overpayment, the Inland Revenue Authority of Singapore (IRAS) will refund the excess amount to your company.