Navigating international tax regulations can be complex, especially for non-U.S. individuals and entities receiving income from U.S. sources. One critical requirement for foreign taxpayers is completing IRS Form W-8, which determines their tax obligations, withholding rates, and eligibility for treaty benefits. Understanding this form is essential for avoiding unnecessary tax withholding and ensuring compliance with U.S. tax laws.

The U.S. government enforces strict tax compliance rules, and Form W-8 serves as a key document. Without this form, businesses and individuals may face higher withholding rates, potentially affecting cash flow and financial planning.

Form W-8 is not a single document but a series of forms, each catering to specific scenarios. These forms help distinguish between individuals, businesses, and financial intermediaries, ensuring accurate tax reporting and compliance. Whether you are a freelancer working for a U.S. company, a foreign corporation with U.S. clients, or an intermediary handling U.S.-sourced payments, understanding which version of Form W-8 to file is crucial.

In this guide, we will explore the different types of Form W-8, their specific purposes, and the steps required to complete and submit them correctly. Whether you are new to international taxation or looking to refine your tax documentation processes, this guide will provide the essential information needed for smooth compliance with U.S. tax regulations.

You can always book a call with Commenda for expert assistance.

What is Form W-8?

Form W-8 is a series of IRS forms used by foreign individuals and entities to certify their non-U.S. status for tax purposes and claim exemptions from U.S. tax withholding. These forms help determine whether income received from U.S. sources is subject to withholding tax and at what rate. Common versions include W-8BEN for individuals and W-8BEN-E for entities.

W-8 Form Example:

Consider a freelance software developer in India who provides services to a U.S.-based client. Without submitting a W-8BEN form, the client may withhold 30% of the payment as tax. However, by completing the form and claiming treaty benefits, the developer may qualify for a reduced withholding rate or exemption.

What Purpose Does Form W-8 Serve in International Taxation?

Form W-8 plays a vital role in international tax law by helping foreign taxpayers declare their tax residency and claim treaty benefits.

- Importance for non-U.S. individuals and entities: Ensures correct tax withholding and prevents unnecessary deductions.

- Impact on U.S. tax withholding requirements: Helps U.S. businesses comply with IRS regulations when making payments to foreign persons.

Where to Find the W-8 Form?

The latest versions of Form W-8 can be found on the IRS website. Taxpayers must ensure they use the most updated version to remain compliant.

Download W-8 Form Instructions 2025: IRS W-8 Forms and Instructions

Which W-8 Form Should I Use? Different Types of Form W-8

Choosing the correct Form W-8 depends on your status as an individual or entity, the nature of the income you receive, and whether you qualify for tax treaty benefits. Below is a breakdown of the different types of Form W-8, their specific purposes, and when to use them.

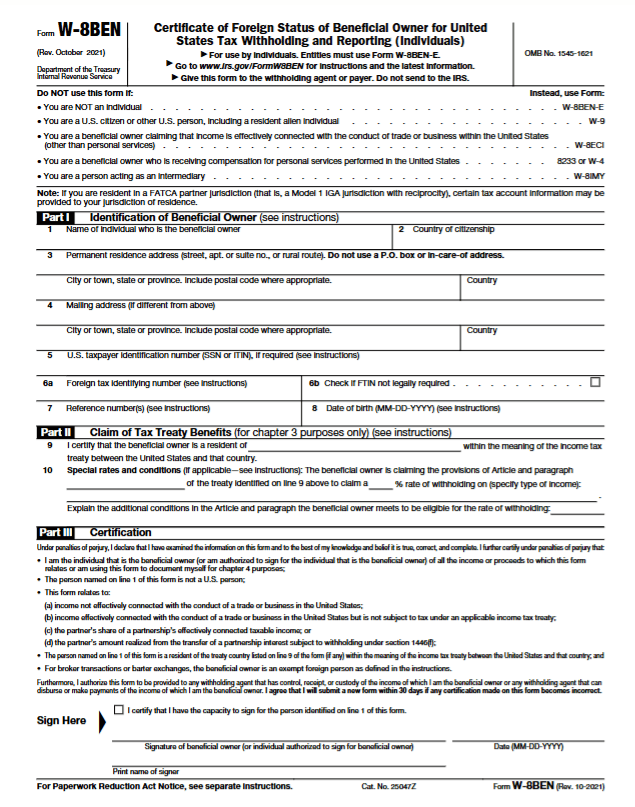

1. W-8BEN:

Form W-8BEN is a Certificate of Foreign Status of Beneficial Owner for U.S. Tax Withholding and Reporting (Individuals)

Who Should Use It?

- Foreign individuals receiving U.S.-sourced income such as dividends, royalties, interest, or freelance payments.

- Non-U.S. residents who want to claim reduced withholding rates under a tax treaty.

Form W-8BEN Example:

A freelance graphic designer based in Germany receives payments from a U.S. client. Without submitting Form W-8BEN, the client would be required to withhold 30% of the payment for tax purposes. However, since Germany has a tax treaty with the U.S., the designer can use Form W-8BEN to claim a reduced withholding rate.

2. W-8BEN-E:

Form W-8BEN-E is a Certificate of Foreign Status of Beneficial Owner for Entities

Who Should Use It?

- Foreign corporations, partnerships, or other entities receiving U.S.-sourced income.

- Foreign businesses that want to claim tax treaty benefits.

Form W-8BEN-E Example:

A Canadian software company licenses its software to a U.S. business. The company submits Form W-8BEN-E to claim reduced withholding rates on royalty payments under the U.S.-Canada tax treaty.

3. W-8ECI:

Form W-8ECI is a Certificate of Foreign Person’s Claim That Income Is Effectively Connected with the Conduct of a Trade or Business in the U.S.

Who Should Use It?

- Foreign individuals or businesses that earn income directly tied to a trade or business conducted within the U.S.

- Those who need to report their U.S.-sourced income on a tax return rather than be subject to withholding.

Form W-8ECI Example:

A French consulting firm has a U.S. branch office that actively engages in business operations within the U.S. Since their income is “effectively connected” to U.S. trade, they must file Form W-8ECI to report and pay taxes on their earnings.

4. W-8EXP:

Form W-8EXP is a Certificate of Foreign Government or Other Foreign Organization for U.S. Tax Withholding and Reporting

Who Should Use It?

- Foreign governments, international organizations, tax-exempt organizations, and foreign central banks claiming tax exemption under U.S. law.

Form W-8EXP Example:

A foreign university receives grants from U.S. sources to fund research programs. Because it qualifies as a tax-exempt entity, the university submits Form W-8EXP to certify its tax-exempt status.

5. W-8IMY:

Form W-8IMY is a Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches

Who Should Use It?

- Foreign financial institutions, foreign partnerships, or trusts that act as intermediaries for U.S.-sourced payments.

- Entities that receive U.S. income on behalf of others and distribute it accordingly.

Form W-8IMY Example:

An international investment fund collects dividends from U.S. companies and distributes them to investors worldwide. The fund files Form W-8IMY to certify its intermediary status and ensure proper tax withholding for its investors.

What Information Do You Need to Complete Form W-8?

Basic Information Required to File W-8 Form

- Name, address, and country of citizenship.

- Foreign Tax Identification Number (TIN), if applicable.

Additional Details for Each W-8 Form

- W-8BEN: Foreign status declaration, tax treaty claim, and signature.

- W-8BEN-E: Entity classification, withholding agent details.

- W-8IMY: Intermediary and flow-through details.

Special Considerations

- Proof of foreign status (e.g., foreign tax identification numbers, passport, or residency documentation).

How to Successfully Complete and Submit Your W-8 Form?

To successfully complete and submit your W-8 form, follow these 4 step guide to filling out the W-8 Form:

Step 1: Identify the correct form based on your tax status

- If you are an individual, you will typically use Form W-8BEN.

- If you are a foreign entity, Form W-8BEN-E is required.

- If you have effectively connected income (ECI), Form W-8ECI applies.

- If you are an intermediary or tax-exempt organization, Form W-8IMY or W-8EXP may be needed.

- Choosing the right form is crucial to ensure proper tax treatment and avoid unnecessary withholding.

Step 2: Provide accurate personal or entity details

- Fill in your full legal name as it appears on official tax documents.

- Include your permanent residence address, which must be outside the U.S.

- If applicable, provide your Foreign Tax Identification Number (FTIN) or a U.S. TIN if required.

- Specify your country of citizenship or tax residency.

Step 3: Claim applicable tax treaty benefits if eligible

- If your country has a tax treaty with the U.S., you may be eligible for reduced withholding rates.

- Complete the appropriate sections of the form to claim these benefits.

- Provide additional documentation if required, such as a residency certificate.

Step 4: Sign and date the form

- Your signature certifies that all information provided is accurate.

- Unsigned or improperly signed forms will be rejected, leading to unnecessary withholding.

Submission Options for W-8 Form

- Paper Filing: Some withholding agents require physical submission. Ensure you send it to the correct department.

- Electronic Filing: Many financial institutions and businesses accept digital submissions through secure portals.

Avoiding Common Mistakes

- Ensure all required fields are completed.

- Double-check tax treaty eligibility before claiming benefits.

- Keep a copy of the submitted form for your records.

- Update your form if your tax status or address changes.

Mistakes are common but with Commenda experts can help you along the way to reduce compliance costs. Book a call today to understand in detail and avoid common mistakes.

Understanding Special Considerations for Form W-8 Filing

Form W-8 is not just about declaring foreign status, it also plays a crucial role in determining eligibility for tax treaty benefits, handling income that is effectively connected to U.S. trade, and ensuring proper documentation for intermediaries. Understanding these special considerations helps prevent unnecessary tax withholding and ensures compliance with U.S. tax regulations.

How Tax Treaties Impact Your Form W-8 Filing?

The United States has income tax treaties with many countries that provide reduced withholding tax rates on specific types of income, such as dividends, interest, and royalties. These treaties help prevent double taxation by allowing foreign taxpayers to claim benefits based on their residency.

Benefits of Tax Treaties:

✔ Lower withholding rates on eligible income

✔ Avoidance of double taxation

✔ Better cash flow management for foreign businesses and individuals

How to Claim Treaty Benefits on Form W-8?

- Check the applicable tax treaty

- Review the tax treaty between your country and the U.S.

- Determine the applicable withholding tax rate based on your type of income.

- Provide your foreign tax identification number (TIN)

- Some tax treaties require a Foreign Taxpayer Identification Number (TIN) to claim benefits.

- If your country does not issue TINs, you may need to provide alternative proof of tax residency.

- Complete the necessary sections of Form W-8

- Fill out the tax treaty claim section, including the article number under which you are claiming benefits.

- Provide a valid reason for claiming the reduced tax rate or exemption.

Effectively Connected Income (ECI) and Its Impact on Form W-8 Filing

Some foreign individuals and entities earn income that is directly connected to a U.S. trade or business. This income is classified as Effectively Connected Income (ECI) and is taxed differently from passive income like dividends or interest.

What qualifies as ECI?

- Income from actively conducting business in the U.S.

- Rental income from U.S. properties (if the taxpayer elects to treat it as ECI).

- Service-based income earned while physically working in the U.S.

Key Forms Required:

- Form W-8ECI: Used to certify that income is effectively connected with U.S. trade or business.

- Form 1040NR (Nonresident Alien Income Tax Return): Required for individuals to report ECI and pay U.S. income tax.

Handling Foreign Intermediaries and Flow-Through Entities

Certain foreign entities, such as intermediaries, partnerships, and flow-through entities, receive U.S.-source income on behalf of others. These entities must file Form W-8IMY to properly allocate tax withholding among their underlying beneficiaries.

When to use Form W-8IMY?

✔ If you are a financial institution, such as a foreign bank or investment fund, receiving payments on behalf of clients.

✔ If you are a foreign partnership distributing income to multiple partners.

✔ If you are a foreign trust acting as an intermediary for beneficiaries.

Reporting Requirements for Intermediaries

- Must provide withholding statements listing the ultimate beneficiaries of the income.

- Must comply with FATCA (Foreign Account Tax Compliance Act) rules if applicable.

- May be required to withhold tax on payments made to underlying recipients.

Decision Framework to Determine Proper Tax Filing Documentation

Use this checklist to decide which W-8 form to file:

- Are you an individual or an entity?

- Do you have U.S.-connected income?

- Are you claiming treaty benefits?

How to Maintain Form W-8 Compliance and Follow Best Practices?

1. Form W-8 Validity and Renewal Requirements

- Most W-8 forms are valid for three years.

- Renew before expiration to maintain compliance.

2. Documentation Maintenance Strategies

- Store copies of submitted W-8 forms securely.

- Track expiration dates and file renewals on time.

2. Penalties and Consequences for Non-Compliance

- Failure to file: 30% withholding tax may be applied.

- Incorrect information: May lead to penalties or IRS audits.

4. Best Practices for Ongoing Compliance

- Regularly review tax regulations.

- Keep records of all submitted W-8 forms.

- Train personnel handling tax compliance.

Choose Commenda for ensuring a timely and smooth compliance process.

Failing to submit Form W-8 can result in higher tax withholding and loss of treaty benefits.

Possible Consequences:

- Automatic 30% withholding tax on U.S.-source income.

- Loss of tax treaty benefits, meaning higher tax rates apply.

- Delays in payment processing, as withholding agents may require the form before releasing funds.

- IRS audits and compliance issues if incorrect or missing forms trigger an inquiry.

Conclusion

Filing IRS Form W-8 correctly is essential for foreign taxpayers receiving U.S.-sourced income. By understanding the different W-8 forms, tax treaty benefits, and compliance requirements, individuals and entities can avoid unnecessary tax withholding and ensure smooth financial operations.